Assuming there was a company which had developed and patented a technology which resulted in a resolution of a major worldwide problem. The company’s technology has only been proven in verifiable laboratory experiments. Commercial exploitation of the technology requires construction and operation of a demonstration plant. The company believes that it will require two years to build the plant and commence operations. The company believes the plant will be highly profitable and will demonstrate the replicability of the necessary technology. The company already has orders for three of its units priced at $8.0 million each. The market demand for the unit are expected to be vast as the problem solved by the technology is widespread.

The company seeks to place with an investor a ten-year, five percent of revenues royalty for $5.0 million. However, the royalty will have an issuer’s right of redemption permitting termination of the royalty upon the payment of $15.0 million to the investor if within 36 months or $25.0 million if within 60 months. The 36-month Internal Rate of Return (IRR) would be at least 44% and if five times the investor’s cost of the royalty in five years, at least a 38% IRR. The reason for being only able to calculate the minimum IRR is that the royalties will be paid whenever the company receives revenue and there is an assumption the received royalty payments will be reinvested for some return.

The issuer’s right of redemption is one of the unique terms included in the royalties we structure and recommend. It is this investor’s favorable return arrangement which also attracts issuers because they have the ability to terminate the royalty payment obligation.

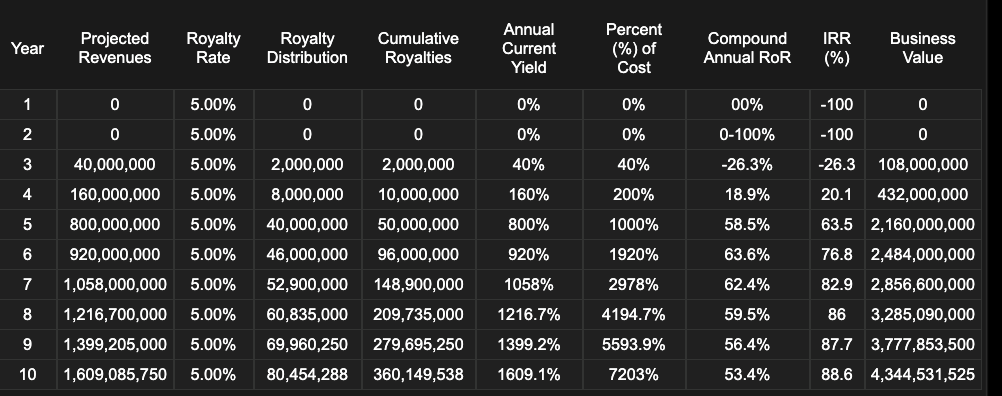

In the following analytics table for the described company, assuming the achievement of the revenues projected, the issuer’s saving of royalty payments would be $345 million, and if for the five-year redemption payment of $25 million the issuer’s saving would be $310 million. It is reasonable that the issuer, on the achievement of the projected revenues, would have the ability to raise the necessary redemption amount in the earlier period and the investor would already have received the $25 million redemption value in the payment of royalties within the fifth year.

From the investor’s perspective it is revenue projection of $40 million in the third year which has to be found realistic as the nature of the product produced by the company’s technology is such that which makes the projections both possible and assures the exercise of the issuer’s right of redemption.

The following analytics table is based solely on the revenue projections submitted by the prospective royalty issuing company. The assumptions were that the revenues would have Compound Annual Growth Rate of 15% in the final 5 years after the revenues projected by the company, an 18% Net After Tax Return and a P/E of 15. Of course, none of the statistics are expected to be significant to the royalty investor as the expectation is that the royalty will be redeemed. It is also reasonable to assume the company will be sold for a great deal of money to a major international company.

The purpose of describing this one opportunity is to highlight the importance to both the royalty issuer and the royalty investor of negotiating the royalty issuer’s right of redemption terms. Royalties have the ability to be both fair and attractive to both parties in a transaction. However, it is the issuer’s right of redemption which attracts those companies having outstanding undeveloped assets to use royalties as a means of obtaining the necessary capital on terms which are also attractive to income seeking investors.

To learn more, please review the postings in arthurlipper.com and study REX-Basic.com.

Arthur Lipper, Chairman

British Far East Holdings Ltd.

chairman@REXRoyalties.com

+1 858 793 7100

© Copyright 2020 British Far East Holdings Ltd. All rights reserved.

Blog Management: Viktor Filiba

termic.publishing@gmail.com