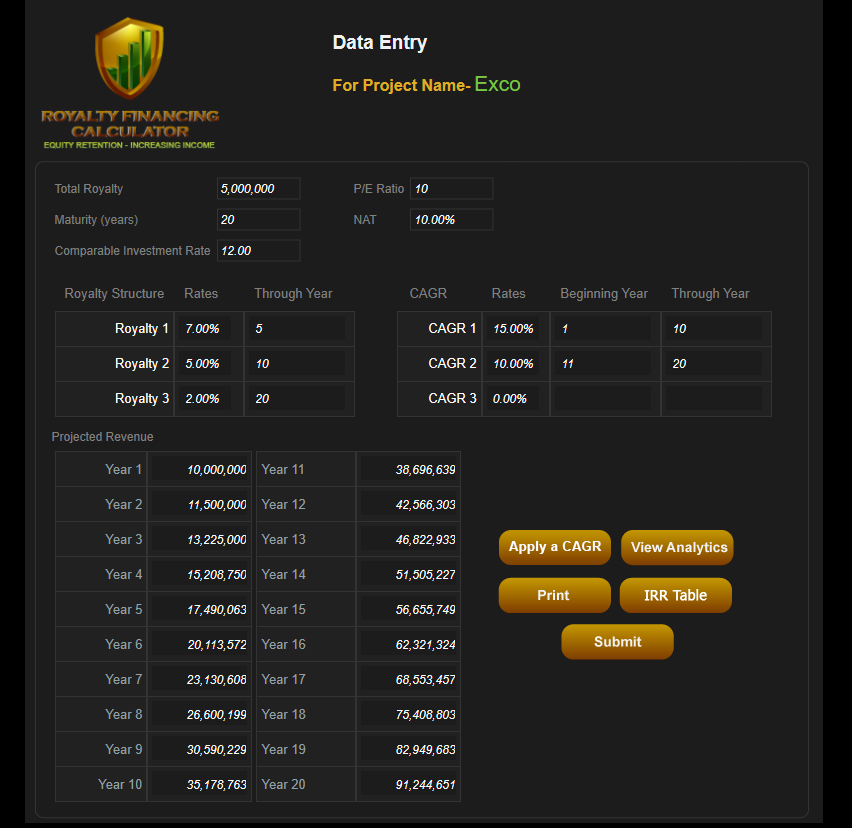

A closely held, privately-owned company, Exco, is seeking $5 million through issuing a revenue royalty, used to finance either an acquisition or business investment aimed at generating an immediate increase in revenues.

Exco has been in business for more than 6 years and has been profitable, with increasing revenues, for the last 3 years. The revenues for the current year will be $10 million. The Compound Annual Growth Rate (CAGR) for each of the approaches described below is assumed to be the same. Exco has and expects to continue to have at least a 20% pre-tax and 10% Net-After-Tax profit margin. Similar, publicly traded companies in the same industry experience a price/earnings ratio of 10 times per-share profits.

Following are the terms which may theoretically negotiated for a $5 million royalty using three of our different approaches. The Data Entry and Analytics pages generated by our Royalties Analytical System for each follow. The approaches are:

REX-Basic.com, the least complicated, a royalty sold for an agreed amount, at an agreed royalty rate for an agreed period REXdebt-shareRoyalties.com, whereby the royalty issuer first borrows $5 million from either the royalty investor or another lender on terms 30% higher than current commercial lender’s prime interest rates, with a royalty rate reflecting the greatly reduced capital risk to commence on the repayment of the loan, and

REX-RIAR.com (Royalty Issuer Assured Royalty), in which the company issuing the royalty (or a credible third-party) assures the royalty investor (with either internal assets or through a third-party assurance) of a minimum payment of royalties for an agreed period or periods. The REX-RIAR approach also introduces the concept of a Credited Royalty (amount of royalty payments being retained by the issuer until maturity of the royalty payment period) as well as displaying the results for the conventionally Distributed Royalty.

The Royalties Analytic System is described in some detail at http://royalties.website, with individual links to each component of the system.

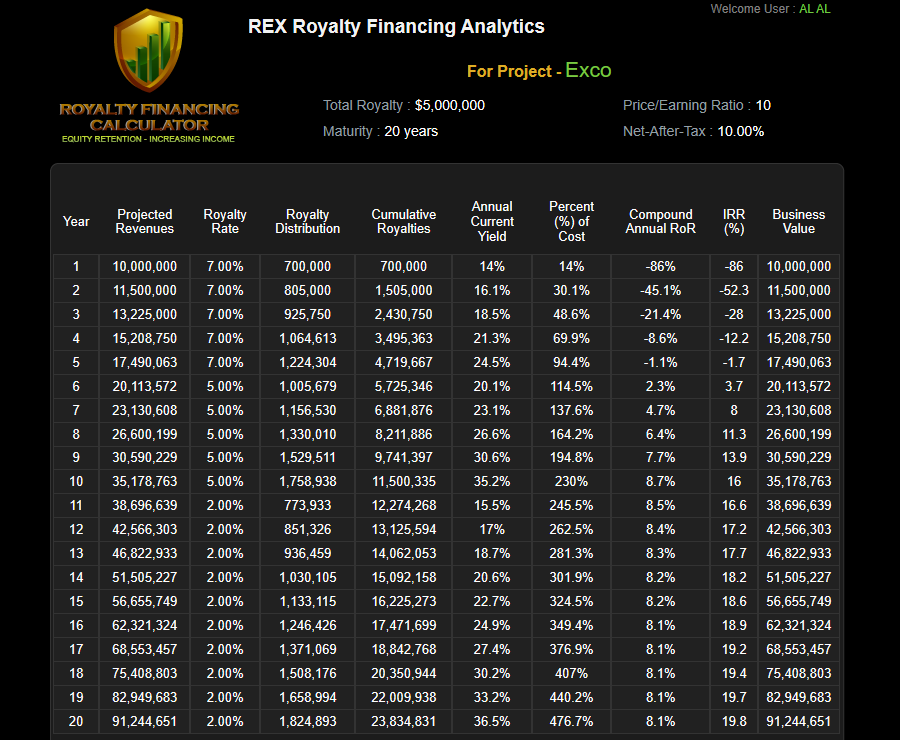

This is the basic Exco Case Study, and its revenue assumptions remain constant in the other two cases. The Royalty Rate, beginning at 7% and decreasing in subsequent periods to 5%, and then 2%, would result in the following anticipated returns to investors, if the projected revenues are achieved.

Investors would receive all their original capital back in just over 5 years, from the cumulative stream of revenue royalties distributed quarterly. The Internal Rate of Return (IRR) for the investment would be 16% over the first 10 years, rising gradually to nearly 20% over the full 20-year term.

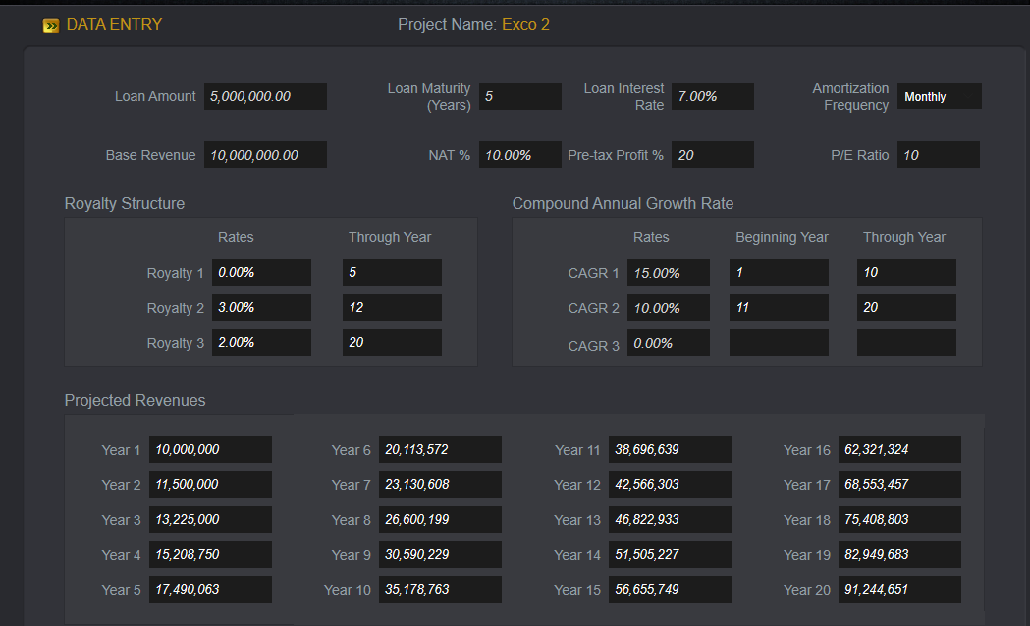

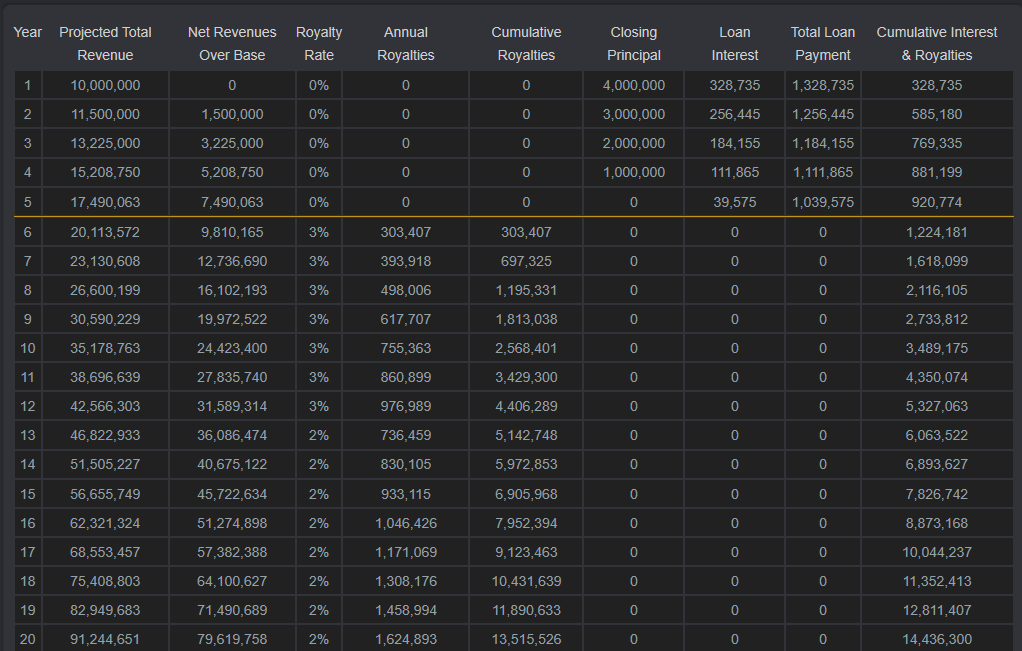

REXDEBT-SHAREROYALTIES.COM = Exco 2

In the Exco 2 Case Study, the investment begins with a short-term debt at 7%, which converts to revenue royalties after the 5th year. Using the same revenue assumptions, but with lower royalty rates beginning at 3% and then decreasing to 2%, the IRR at the end of 20 years would be very similar in both Exco 1 and Exco 2, and the investor would have zero capital risk after the 5th year because by that time the original investment principal has been returned.

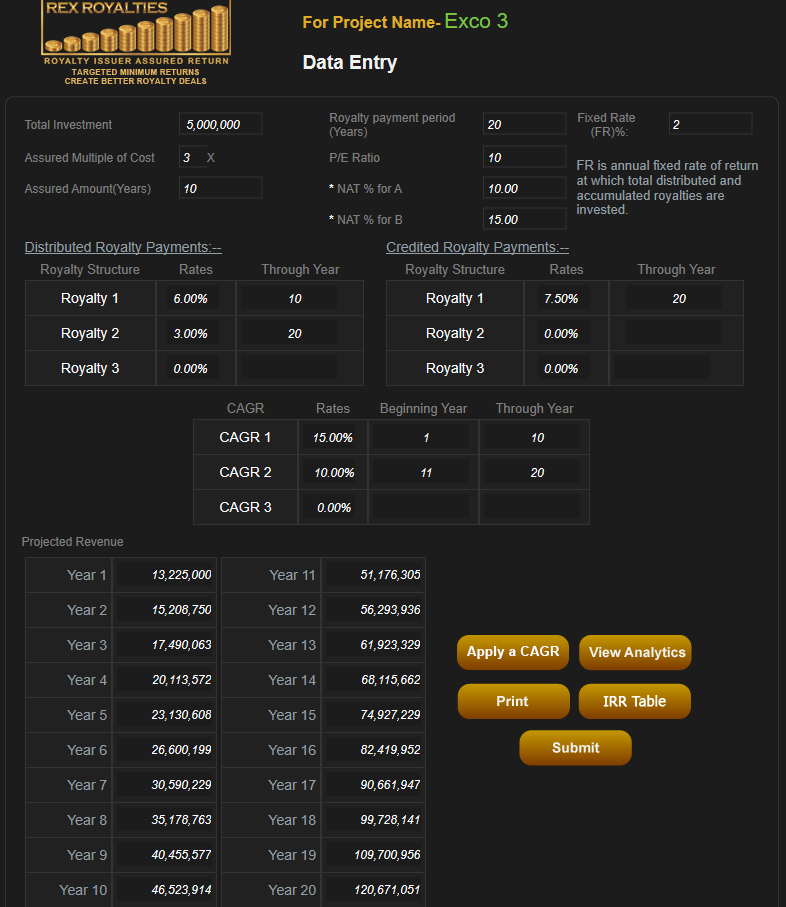

REX-RIAR.com – Exco 3

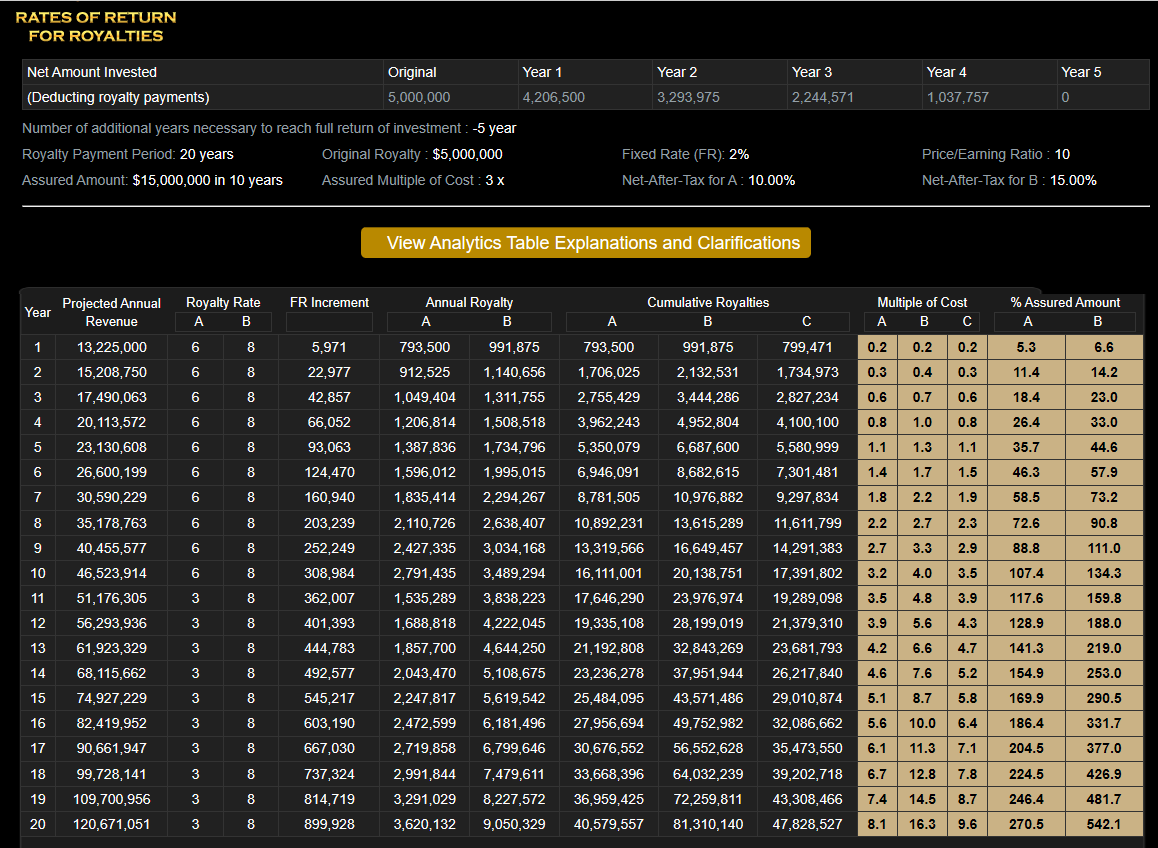

In the Exco 3 case study, all revenue and other key metrics remain the same as in Exco 1 and Exco 2. However, investors are assured of a minimum of 3 times their initial cost; and royalties generated are not distributed by the company, but retained and reinvested on behalf of investors at 2% annual return. The break-even point remains the same (about 5 years), but anticipated IRR after 10 years is 28.1%, and after 20 years IRR rises to 33.2%, when the final accumulated payout to investors is made.

There is so much in the RIAR approach benefiting both investors and royalty issuers that I believe it will ultimately become the structuring standard.

It is important to remember that in each of the approaches the royalty issuing company would have, as we recommend, a right of redemption permitting the termination of the royalty on pre-agreed terms, resulting in returns for the investor substantially exceeding the investor’s initially targeted IRR.

I will be pleased to chat with those having questions or observations re the Analytics or the Data Entry for each of the three approaches.

Arthur Lipper, Chairman

British Far East Holdings Ltd.

chairman@REXRoyalties.com

+1 858 793 7100

* Michael J. North, my friend and partner in both China Royalties and Pacific Royalties, frequently helps me by editing and contributing to articles such as this Case Study describing three of our approaches for using revenue royalties in the financing of company revenue growth. I thank Michael and recognize the help he has provided.

© Copyright 2019 British Far East Holdings Ltd. All rights reserved.

Blog Management: Viktor Filiba

termic.publishing@gmail.com